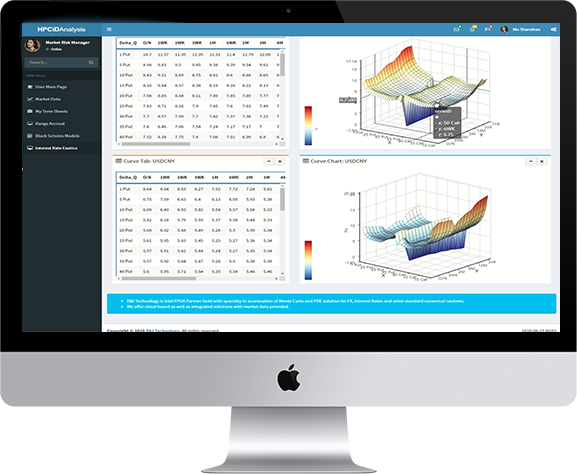

Taking advantage of HPCiD's excellent parallel computing performance, D&I developed its own set of derivatives pricing models, adopted a client risk framework and model governance, and implemented them in Python, C++ or C#. How all pricing models work is fully transparent and easy to audit. Models covered by the D&I Model Library include but are not limited to:

Our model covered includes:

1. 1- and 2- factor Hull-White model;

2. Cross Currency Hull-White model;

3. Single currency and cross currency Libor Market Model;

4. Black-Scholes-Merton model;

5. Bachelier model;

6. Equity local volatility model, a.k.a Dupire model;

7. FX local volatility model;

8. Heston model;

9. SABR smile interpolation.

10. Deterministic hazard rate model.

Our product coverage includes:

1. All linear rates, fx products;

2. First generation FX and Equity products, e.g. barriers and touches;

3. Sophisticated interest rates exotics like Bermudan, Callable Range Accrual;

4. Popular in Asia FX structures like TARN variants, Accumulators, Pivots;

5. Popular equity structures like Accumulators, Basket options with memories.

We can adopt customer risk framework and model governance, and implement in Python, C++, or C#. Our work is fully transparent and easily auditable.

Online

Services

On-lineService Time: 9:00-18:00